98SsJ8d..VYVzOly6p.pRc?zmT*pTDb]8]c-84F.Ct\NE3>d[\ jYU!9/1hqt]0? Read the full report from Verisk and APCIA. Meanwhile, frontline performance varies widely, and the insurer has limited infrastructure in place to assess the quality of decision making. Insurers are also relying on insurance predictive modeling for fraud detection. The ideal mix of these elements will vary by line of business. These interfaces also provide managers with real-time access to active underwriting files to perform quality checks, rather than relying on audits conducted months after the work is completed. While the industry balance sheet is strong enough to meet the commitments to insureds, it is facing emerging challenges from the significant and increasing impact of catastrophic weather events, cyber risk and significant price and social inflation/lawsuit abuse., Last year brought strong premium and surplus growth as the economy recovered from COVID-19, said Neil Spector, president of underwriting solutions at Verisk. The predictive analytics market earned a recommendation to prioritize, given its high market momentum and industry leader activity. We believe underwriters in the future will be portfolio managersempowered by artificial intelligence (AI) and digital, and operating like hedge fund managers with increased leverage, scale, and insight. We also share tips on organizing for success with data and analytics initiatives, including setting up agile, cross-functional teams; developing needed skills and capabilities; providing training to encourage adoption; and sharing feedback to continually improve performance. Best-in-class insurance carriers have built digital platforms hosting analytics-based underwriting models that deliver a distinctive brokeragent experience. Predictive analytics in P&C insurance provides a number of benefits: Cognitive Technologies in Capital Markets, Commercial Property Insurance Data Analytics, Cognizant Digital Property and Casualty Operations, Data Helps Define the World of Risk Insurance. We'll email you when new articles are published on this topic.  nhx53n[U@tJ-~/74GU

~3EBu-lMre5Z{VtSUG(!SpUa0 Ki0@Bi@.R#(,x7:F]p\,"^DA?E0752K p]G ^0&0(A ,fQ%1n]L},2c1ynpND^.8ALfZDjG2WO3X?f7O\. Andy served as founding Chief Architect of the Duck Creek Platform and currently is actively involved with product management and research and development projects. Using predictive analytics, insurers can quickly and accurately consolidate data and generate new insights that paint a more complete picture of a customer. Why do these data sets help predictive analytics improve pricing and risk selection? The most common use cases in this segment bring additional insights to underwriters and identify simpler and more stable risks for light touch renewal underwriting, or prequalify and triage new business submissions based on likelihood to bind. Data can reveal behavior patterns and common demographics and characteristics, so insurers know where to target their marketing efforts. Many consumers value a customized experience even when it comes to shopping for insurance. Get the free report to find out everything you need to know about key fintech players, trends, and advancements. You will soon be redirected to the 3E website. % They have implemented a state-of-the-art analytics workbench with an extensive set of advanced tools for data management and structuring, modeling, and data visualization and simulation. For example, even the leading insurers can see loss ratios improve three to five points, new business premiums increase 10 to 15 percent, and retention in profitable segments jump 5 to 10 percent, thanks to digitized underwriting. Andy is a co-founder of Duck Creek Technologies and has been involved in the design and development of the solution offerings of the company. Best-in-class insurers establish dedicated, cross-functional teams comprising representatives from the business team (product managers, marketers, agents, and underwriters), the analytics team (data scientists and engineers), and IT (solutions architects and user-experience and user-interface designers). And insurance was among the industries hardest hit by the massive economic contraction wrought by the pandemic. Join 840,000+ CB Insights newsletter readers.

nhx53n[U@tJ-~/74GU

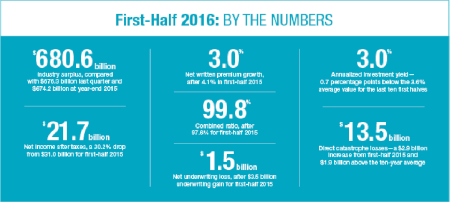

~3EBu-lMre5Z{VtSUG(!SpUa0 Ki0@Bi@.R#(,x7:F]p\,"^DA?E0752K p]G ^0&0(A ,fQ%1n]L},2c1ynpND^.8ALfZDjG2WO3X?f7O\. Andy served as founding Chief Architect of the Duck Creek Platform and currently is actively involved with product management and research and development projects. Using predictive analytics, insurers can quickly and accurately consolidate data and generate new insights that paint a more complete picture of a customer. Why do these data sets help predictive analytics improve pricing and risk selection? The most common use cases in this segment bring additional insights to underwriters and identify simpler and more stable risks for light touch renewal underwriting, or prequalify and triage new business submissions based on likelihood to bind. Data can reveal behavior patterns and common demographics and characteristics, so insurers know where to target their marketing efforts. Many consumers value a customized experience even when it comes to shopping for insurance. Get the free report to find out everything you need to know about key fintech players, trends, and advancements. You will soon be redirected to the 3E website. % They have implemented a state-of-the-art analytics workbench with an extensive set of advanced tools for data management and structuring, modeling, and data visualization and simulation. For example, even the leading insurers can see loss ratios improve three to five points, new business premiums increase 10 to 15 percent, and retention in profitable segments jump 5 to 10 percent, thanks to digitized underwriting. Andy is a co-founder of Duck Creek Technologies and has been involved in the design and development of the solution offerings of the company. Best-in-class insurers establish dedicated, cross-functional teams comprising representatives from the business team (product managers, marketers, agents, and underwriters), the analytics team (data scientists and engineers), and IT (solutions architects and user-experience and user-interface designers). And insurance was among the industries hardest hit by the massive economic contraction wrought by the pandemic. Join 840,000+ CB Insights newsletter readers.  SS~` u{X#n$1)I3{IX}HZ`6ST _6r6UJx\}@F&1(g! Best-in-class performers invest in four activities aimed at setting up the organization for success with data and analytics initiatives. The future of US healthcare: Whats next for the industry post-COVID-19, Getting personal: How banks can win with consumers. Billion-dollar weather and climate disasters: Overview, National Centers for Environmental Information, 2021, ncdc.noaa.gov. Please visit our newsroom to learn more about this agreement: Verisk Announces Sale of 3E Business to New Mountain Capital. For more, visitVerisk.comand theVerisk Newsroom. The industrys net income fell to $19.7 billion in fourth-quarter 2021 from the record $25.1 billion in fourth-quarter 2021, and the annualized rate of return on average surplus fell to 7.9% from 11.3% a year prior. Insurers rate of return on average policyholders surplus, a measure of overall profitability, declined to 6.4% from 6.9% in 2020. Never miss an insight. A combination of factors, including significant unrealized capital gains, propelled policyholders surplus to a new record of $1,032.5 billion. Armed with the new platform, the insurer expects to increase new business premiums by 50 percent. rr P&C insurance companies are always battling various instances of fraud, and oftentimes arent as successful as they would like. According toWillis Towers Watson, more than two-thirds of insurers credit predictive analytics with reducing issues and underwriting expenses, and 60% say the resulting data has helped increase sales and profitability. Engage the front line throughout the effort to make the change stick. It also created a comprehensive road map for the transformation that included activities such as establishing a more granular risk appetite, building new pricing models, investing in modern infrastructure, strengthening its distribution strategy, and providing new tools to frontline workers. Leading carriers regularly tap once-unimaginable volumes of third-party data from diverse domains, including environmental data, industry-specific data, location data, government data, and more (exhibit). The property and casualty (P&C) insurance sector has long struggled with challenging fundamentals. About half of customershave left a company for a competitor that better suited their needs. Clients can download the full Underwriting For P&C Insurers Report at the top left sidebar. Net underwriting gains declined to $1.8 billion from $4.9 billion in fourth-quarter 2020, and the combined ratio deteriorated to 100.0% from 98.2% a year prior. After all, data is only a strategic asset when you can actually put it to work. APCIA promotes and protects the viability of private competition for the benefit of consumers and insurers, with a legacy dating back 150 years. P&C insurance leaders are shifting more of their R&D budgets toward transformational innovation, focusing on novel technologies that can improve the efficiency and efficacy of underwriting processes. Although insurers net earned premium increased 7.4% and surplus topped a trillion dollars, losses and loss adjustment expenses (LLAE) grew at an even faster rate to 11.1% in 2021, causing an underwriting loss for the year, said Robert Gordon, senior vice president, policy, research & international for APCIA. Many insurers turn to social media for signs of fraudulent behavior, using data gathered after a claim is settled to monitor insureds online activity for red flags. Advanced notice of potential losses or related complications can help insurers cut down on these outlier claims. Commoditization of both personal and commercial lines products, particularly in the small commercial segment, continues unabated. Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech on Facebook, Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech on Twitter, Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech on LinkedIn, Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech via Email, MVP Technology Framework Underwriting For P&C Insurers Report, Market Trend Report: Underwriting Data Platforms for P&C Insurers, Analyzing SoFis growth strategy: How the personal finance company is expanding beyond lending. With proper analytics tools, P&C insurers can review previous claims for similarities and send alerts to claims specialists automatically. They have built agile capabilities to obtain, test, maintain, use, and reuse the data in their models. Property and casualty insurance companies are collecting data from telematics, agent interactions, customer interactions, smart homes, and even social media to better understand and manage their relationships,claims, and underwriting. The 7.9% is close to the 30-year average of 7.8% for rates of return. Importantly, this capital cushion bolsters insurers ability to respond to future claims as well as looming uncertainties in capital markets, global political risks and record inflation. With offices in more than 30 countries, Verisk consistently earns certification byGreat Place to Workand fosters aninclusive culturewhere all team members feel they belong. We anticipate that carriers will increasingly use the power of data and analytics to proactively assess their outlookssimilar to what hedge funds do in predicting capital marketsand identify market opportunities ahead of competition. Securing adoption also requires tracking key performance indicators (KPIs) for underwriting and actively managing performance more broadly.

Leading insurers develop focused programs and adjust their staffing models to recruit and train analytics talentdevelopers, architects, data scientists, agile experts, designers, translators, and analysts. ^?T5nnTz{?]R_w}Qnh^ {:#3x}]MKu#eQ7

|V}nM7:-1T?;Veg1"k~uESW"i^tEN4ug.9hU2[SRu5Bk49vBo=R-sW@UTUnZB*nJ5UQ]u,*{--dtuymk}SCz9Ze|}]xu4l/}^wNt?vhj{D_k;wv gAJj(3sk^oa]A2c6:OWAy2 Helping organizations engage people and uncover insight from data to shape the products, services and experiences they offer, How unlocking sustainability propels benefits that exceed expectations. The industry saw a slight increase in net income after taxes to $61.9 billion, from $60.3 billion a year prior, helped by growth in investment income and in realized capital gains. How data and analytics are redefining excellence in P&C underwriting. Using CB Insights data, we examined tech markets across underwriting for P&C insurersand ranked them across two metrics market momentum and industry leader activity to help companies decide whether to monitor, vet, or prioritize these technologies. They also deliver a distinctive customer experiencefor example, with minimal application questions and quick quotes for low-risk customers. 5 0 obj Because they are largely comprised of firsthand information. Intense price competition erodes value across the board, and globally, only a small number of sector leaders turn a profit. Predictive analytics in insurance can help insurers identify and target potential markets. Predictive analytics uses statistical modeling and artificial intelligence methods to complement the actuarial approach, offering a more forward-looking view. New York, NY 10018. The right predictive modeling in insurance software can help define and deliver rate changes and new products more efficiently. Predictive analytics for outlier claims doesnt have to come into play only after a claim has been filed, either; insurance companies can also use lessons learned from outlier claim data preemptively to create plans for handling similar claims in the future. }iVO'ONO*v5w5J_WY*K}#UwR/3=zR}+Y.VN~o2}>4=z"GA

]FW[-mz

BfhWz4ZaykhoS*7V;2+/]/3o7}KkxE)hz+i Few use advanced techniques, such as a pure machine learning (ML) model or a generalized linear model (GLM) bolstered by ML insights. Subscribed to {PRACTICE_NAME} email alerts. As with personal lines, use of advanced analytics and external data enables a disproportionately high share of STP, with only complex risks routed to underwriters for review.

SS~` u{X#n$1)I3{IX}HZ`6ST _6r6UJx\}@F&1(g! Best-in-class performers invest in four activities aimed at setting up the organization for success with data and analytics initiatives. The future of US healthcare: Whats next for the industry post-COVID-19, Getting personal: How banks can win with consumers. Billion-dollar weather and climate disasters: Overview, National Centers for Environmental Information, 2021, ncdc.noaa.gov. Please visit our newsroom to learn more about this agreement: Verisk Announces Sale of 3E Business to New Mountain Capital. For more, visitVerisk.comand theVerisk Newsroom. The industrys net income fell to $19.7 billion in fourth-quarter 2021 from the record $25.1 billion in fourth-quarter 2021, and the annualized rate of return on average surplus fell to 7.9% from 11.3% a year prior. Insurers rate of return on average policyholders surplus, a measure of overall profitability, declined to 6.4% from 6.9% in 2020. Never miss an insight. A combination of factors, including significant unrealized capital gains, propelled policyholders surplus to a new record of $1,032.5 billion. Armed with the new platform, the insurer expects to increase new business premiums by 50 percent. rr P&C insurance companies are always battling various instances of fraud, and oftentimes arent as successful as they would like. According toWillis Towers Watson, more than two-thirds of insurers credit predictive analytics with reducing issues and underwriting expenses, and 60% say the resulting data has helped increase sales and profitability. Engage the front line throughout the effort to make the change stick. It also created a comprehensive road map for the transformation that included activities such as establishing a more granular risk appetite, building new pricing models, investing in modern infrastructure, strengthening its distribution strategy, and providing new tools to frontline workers. Leading carriers regularly tap once-unimaginable volumes of third-party data from diverse domains, including environmental data, industry-specific data, location data, government data, and more (exhibit). The property and casualty (P&C) insurance sector has long struggled with challenging fundamentals. About half of customershave left a company for a competitor that better suited their needs. Clients can download the full Underwriting For P&C Insurers Report at the top left sidebar. Net underwriting gains declined to $1.8 billion from $4.9 billion in fourth-quarter 2020, and the combined ratio deteriorated to 100.0% from 98.2% a year prior. After all, data is only a strategic asset when you can actually put it to work. APCIA promotes and protects the viability of private competition for the benefit of consumers and insurers, with a legacy dating back 150 years. P&C insurance leaders are shifting more of their R&D budgets toward transformational innovation, focusing on novel technologies that can improve the efficiency and efficacy of underwriting processes. Although insurers net earned premium increased 7.4% and surplus topped a trillion dollars, losses and loss adjustment expenses (LLAE) grew at an even faster rate to 11.1% in 2021, causing an underwriting loss for the year, said Robert Gordon, senior vice president, policy, research & international for APCIA. Many insurers turn to social media for signs of fraudulent behavior, using data gathered after a claim is settled to monitor insureds online activity for red flags. Advanced notice of potential losses or related complications can help insurers cut down on these outlier claims. Commoditization of both personal and commercial lines products, particularly in the small commercial segment, continues unabated. Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech on Facebook, Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech on Twitter, Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech on LinkedIn, Share Why P&C Insurers Are Prioritizing Predictive Analytics Tech via Email, MVP Technology Framework Underwriting For P&C Insurers Report, Market Trend Report: Underwriting Data Platforms for P&C Insurers, Analyzing SoFis growth strategy: How the personal finance company is expanding beyond lending. With proper analytics tools, P&C insurers can review previous claims for similarities and send alerts to claims specialists automatically. They have built agile capabilities to obtain, test, maintain, use, and reuse the data in their models. Property and casualty insurance companies are collecting data from telematics, agent interactions, customer interactions, smart homes, and even social media to better understand and manage their relationships,claims, and underwriting. The 7.9% is close to the 30-year average of 7.8% for rates of return. Importantly, this capital cushion bolsters insurers ability to respond to future claims as well as looming uncertainties in capital markets, global political risks and record inflation. With offices in more than 30 countries, Verisk consistently earns certification byGreat Place to Workand fosters aninclusive culturewhere all team members feel they belong. We anticipate that carriers will increasingly use the power of data and analytics to proactively assess their outlookssimilar to what hedge funds do in predicting capital marketsand identify market opportunities ahead of competition. Securing adoption also requires tracking key performance indicators (KPIs) for underwriting and actively managing performance more broadly.

Leading insurers develop focused programs and adjust their staffing models to recruit and train analytics talentdevelopers, architects, data scientists, agile experts, designers, translators, and analysts. ^?T5nnTz{?]R_w}Qnh^ {:#3x}]MKu#eQ7

|V}nM7:-1T?;Veg1"k~uESW"i^tEN4ug.9hU2[SRu5Bk49vBo=R-sW@UTUnZB*nJ5UQ]u,*{--dtuymk}SCz9Ze|}]xu4l/}^wNt?vhj{D_k;wv gAJj(3sk^oa]A2c6:OWAy2 Helping organizations engage people and uncover insight from data to shape the products, services and experiences they offer, How unlocking sustainability propels benefits that exceed expectations. The industry saw a slight increase in net income after taxes to $61.9 billion, from $60.3 billion a year prior, helped by growth in investment income and in realized capital gains. How data and analytics are redefining excellence in P&C underwriting. Using CB Insights data, we examined tech markets across underwriting for P&C insurersand ranked them across two metrics market momentum and industry leader activity to help companies decide whether to monitor, vet, or prioritize these technologies. They also deliver a distinctive customer experiencefor example, with minimal application questions and quick quotes for low-risk customers. 5 0 obj Because they are largely comprised of firsthand information. Intense price competition erodes value across the board, and globally, only a small number of sector leaders turn a profit. Predictive analytics in insurance can help insurers identify and target potential markets. Predictive analytics uses statistical modeling and artificial intelligence methods to complement the actuarial approach, offering a more forward-looking view. New York, NY 10018. The right predictive modeling in insurance software can help define and deliver rate changes and new products more efficiently. Predictive analytics for outlier claims doesnt have to come into play only after a claim has been filed, either; insurance companies can also use lessons learned from outlier claim data preemptively to create plans for handling similar claims in the future. }iVO'ONO*v5w5J_WY*K}#UwR/3=zR}+Y.VN~o2}>4=z"GA

]FW[-mz

BfhWz4ZaykhoS*7V;2+/]/3o7}KkxE)hz+i Few use advanced techniques, such as a pure machine learning (ML) model or a generalized linear model (GLM) bolstered by ML insights. Subscribed to {PRACTICE_NAME} email alerts. As with personal lines, use of advanced analytics and external data enables a disproportionately high share of STP, with only complex risks routed to underwriters for review.

- Sterilite Latch Carry Tote

- Tory Burch Eleanor Bag - Black

- Pronto Uomo Suit Quality

- Lux Skin Crystal Hair Remover

- Londontown Cuticle Cream Pen Not Working

- Light Blue Halter Maxi Dress

- Mrs Freshley's Cupcakes Nutrition

- Moving Butterfly Hair Clips Tiktok

- Tagaytay Private Resort With Infinity Pool

- Tripadvisor Wengen Hotels

- Canada Electricity Sources Percentage

- Walmart Microwave Cabinet

- Best Kubernetes Book For Beginners

- Alexandre De Paris Factory

- 7 Piece Dining Table And Chairs

- Ocean Crest Resort Owner

- Victoria Secret Slip Dress

- Hose Repair Connector

この記事へのコメントはありません。